Pakistan Forex Reserves have risen to their highest level since early 2022, signaling improving economic stability and external resilience. The economy of Pakistan has endured extreme pressure throughout a significant part of the last ten years characterized by a high rate of inflation, a huge external debt burden, and recurrent balance of payment crisis. However, in 2025, the nation has scored a significant achievement: the foreign exchange reserves have risen to the maximum since the beginning of 2022, providing a significant insulation against external shocks and an indicator of the deterioration of macroeconomic stability.

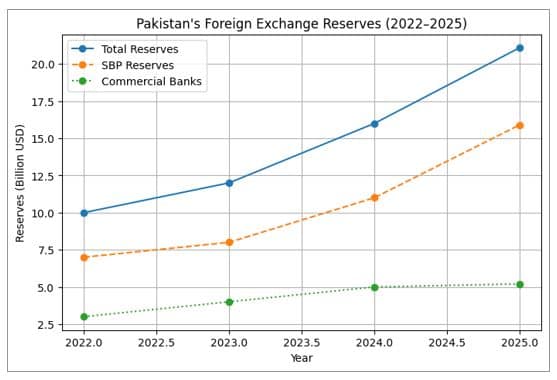

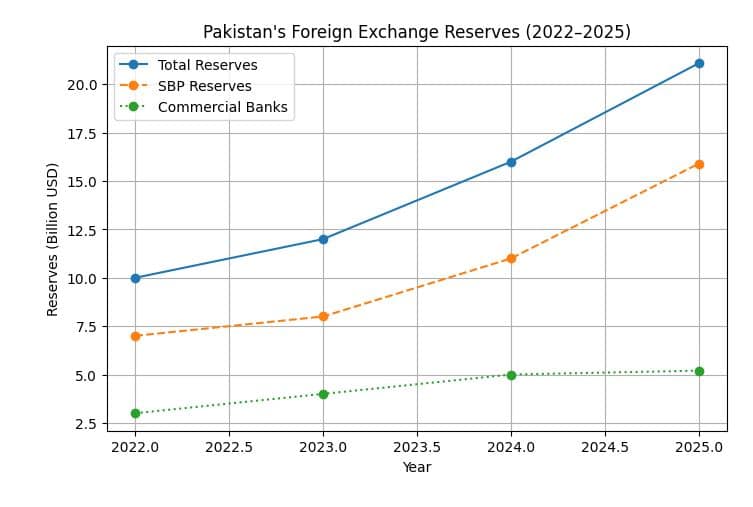

By the middle of December 2025, the amount of liquid foreign exchange reserves of Pakistan was about 21.09 billion. This amount is a mix of foreign exchange held by the State Bank of Pakistan (SBP) which was approximately equal to $15.9billion and by the commercial banks which was approximately equal to 5.2billion.

Why Reserve Levels Matter

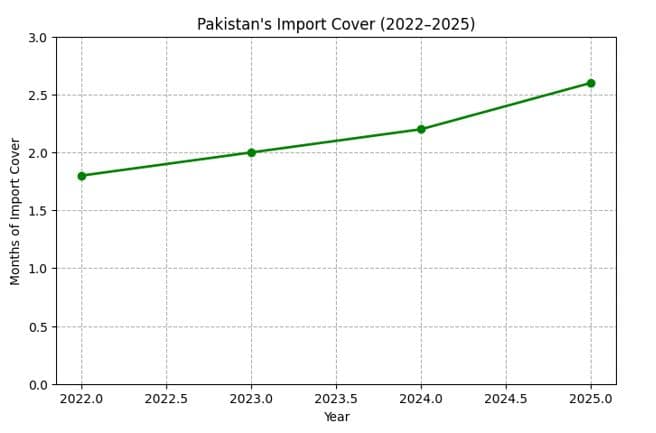

Foreign reserves are used to cushion the countries to settle the necessary imports, as well as, settle the international debts without involving emergency borrowing, or disrupting the exchange rate. Higher reserves, particularly in terms of months of import cover, would indicate that a country is in a better position to resist any form of change in the global markets, that of capital flows, or, in terms of abrupt increase in the prices of imports. Conventionally, policymakers would like to have reserves which are able to take at least three months of imports, but these targets differ depending on a country and the state of its economy.

Recent increase in the reserve of Pakistan allowed the country to cover its imports at some approximately 2.6 months of goods and services by far being at a much higher level than that it was only a few years ago.

How Did Pakistan Reach This Point?

Higher reserves in 2025 did not occur accidentally. Continuity in the macroeconomic policy has helped to support it, a judicious approach to external accounts, and most importantly, specific assistance by international financial institutions. Specifically, Pakistan has been on a multi-year financing deal with the International Monetary Fund (IMF) IMF has been able to finance it through an Extended Fund Facility, with other resources sourced in its Resilience and Sustainability Facility. Some of the most recent disbursements such as a Special drawing fund (SDR) allocation of approximately US $1.2 billion have also contributed significantly to reserve build-ups.

IMF has stressed on the stability that Pakistan has achieved in stabilizing its economy and how its inflation and foreign reserves are improving as part of the whole structural adjustment measures which have been enabled by the bailout program.

Other untied inflows like commercial loans, multilateral funding also assisted at the beginning of the fiscal year 2025, which propelled SBP reserves to surpass IMF projection targets to the tune of more than 14 billion by June 30, 2025, even.

What Has Changed Compared to Past Episodes?

In the past, Pakistan had a challenge of constructing sustainable foreign reserves without involving itself in huge foreign borrowing. During extreme crises in the balance of payment, the reserves held by the State Bank plummeted, did away with the confidence and needed emergency rescue packages by the friendly nations and international financial institutions.

In comparison, however, the latest reserve augmentation does not depend as much on new debt gathering as it does on a compound of policy discipline, as well as foreign financial assistance in organized programs. This has aided in soothing the foreign position of Pakistan without it imposing an overarching rise in net external debt in the short term, a remarkable contrast to other past cycles when reserves were being drawn down despite such high borrowing.

As long as global economic conditions and the price of commodities are uncertain, the current macro policy constitution has helped to stabilize the expectations of the investors and markets, which has led to a more sustainable external buffer.

Better Import Cover, Reduced Pressures on the Rupee

Import cover – a major measure in showing the period in which a country can afford its imports by use of the foreign reserves, is followed closely by the economists and markets. The import cover of Pakistan has been significantly enhanced as at 2025 and this gives the authorities more flexibility to deal with the trade-related payments and external pressure. Although still below the level being desired by some emerging economies, the fact that it has risen to more than 2.6 months is one positive change as compared to the past years.

Broader Economic Context and Challenges

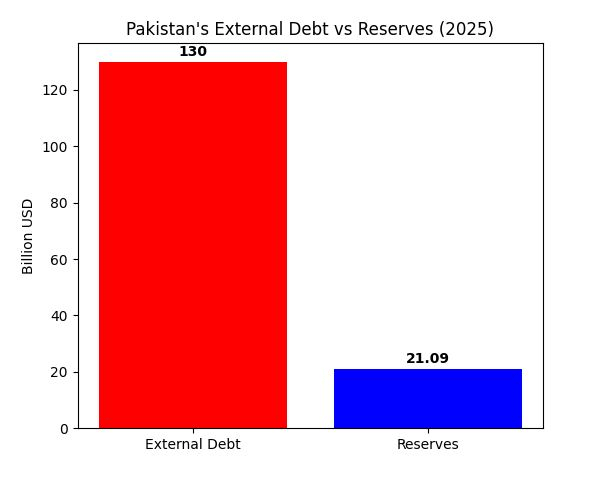

Although there is good news in this, the overall economic situation in Pakistan is complicated. The country still has a heavy load of debt externally, as of late 2025, the country has an external debt of more than 130 billion dollars, the share of which is occupied by the external public debt.

Although the needs of external debt services put strains on the reserves and budget, recent flows have contributed to the removal of the immediate danger of reserves exhaustion. In addition, the interest involvement in international lenders is intended to diversify the maturities and control the cost of financing activities in a more sustainable way in Islamabad.

There has also been the slow growth and the previous pressures of inflation in the economy. The real GDP growth of Pakistan is estimated by the International Monetary Fund at approximately 2.7 in 2025, despite the decrease in the inflation rates, as part of the wider stabilization activities and improvement of the atmosphere in which investments can be made.

What This Means for Pakistan’s Future

The good implication of the existing reserve stance is as follows:

- Less external vulnerability: Even more stock of reserves will allow Pakistan to better absorb the shock of exogenous variations and move around international payment commitments without panic measures.

- Flexibility of policy: As the reserves are higher, listeners allow policy makers more flexibility to use monetary and fiscal policies without worrying that the reserves will run dry.

- Market confidence: oth local and foreign financial markets are most likely to react positively to an evidently greater external buffer. This will sustain inflows of investment and, in the long run, credit ratings.

- Stability in import pay: The presence of better import cover will result in a reduced number of obstacles in the payment of basic goods and services that have to be made, contributing to the stabilization of prices and production.

It is necessary to mention that the reserve accumulation is not an end in itself. Long-term resilience and prosperity require sustainable economic growth; it is a diverse export strategy, foreign direct investment, sound fiscal policy, and industrious sectors. Nevertheless, the recent accumulation of the forex reserves is a notable step towards the continuous economic recovery in Pakistan.

Conclusion

The increase in foreign exchange reserves to a high level since early 2022 is indicative of Pakistan’s proper policy implementation, the systematic involvement of the international financial institutions, and better external flows. Although major issues still prevail, such as huge burden of the debts to the outside world and the ability of the company to grow sustainably, the better buffer in reserve gives more support to the economic stability and trust.

The nature of this period of reserve rebuilt is qualitatively new compared to previous cycles: it is featured by increased reserves and controlled debt pressures, an improved import cover, and a stronger outside position. In case such gains are consolidated due to continuous reforms and sound management of economic progress, Pakistan will be in a better position to overcome the forthcoming global and regional economic hurdles.

Maryam Khalil is an independent writer and BBA student with a strong interest in economy, geopolitics, and environmental issues. Her work offers clear, analytical perspectives on global affairs and emerging trends.